The Economic Storm Ahead: Declining Savings and the Future of Indian Prosperity

- Dr. Anup Kumar Srivastava

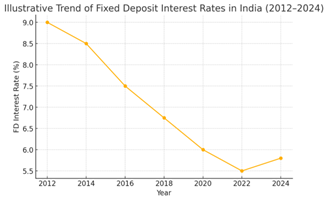

For decades, India’s identity as a nation of savers stood firm. From small town households to urban middle-class families, savings were treated not merely as financial prudence but as a cultural inheritance. This saving mindset protected generations from economic shocks, financed education, supported ageing parents, and ensured upward mobility. However, this foundation is steadily weakening. Today’s policy environment—characterised by falling interest rates, weakened tax incentives for saving, and a growing push toward consumption—has begun to erode the very behaviour that once secured India’s intergenerational stability. If this trend continues, the next generation is likely to inherit a far poorer and more financially vulnerable India. A major turning point in this decline has been the sharp and sustained fall in interest rates on traditional saving instruments. Bank deposits, which hold nearly 60% of household financial wealth in India, no longer offer returns that beat inflation. In the early 2010s, fixed deposits routinely earned around 9–10%, giving savers a meaningful real return on their money. Over the years, however, these rates have steadily fallen. The following figure illustrates the downward drift in fixed deposit rates over the last decade (see Figure 1). When interest rates fall below inflation, savers effectively lose money in real terms, reducing the incentive to keep money in safe, long-term instruments. For middle-class families, senior citizens, and low-income groups—those who rely most on deposits for financial security—this is not just a loss of income but a loss of dignity and future stability.

Figure 1. Illustrative Trend of Fixed Deposit Interest Rates in India (2012–2024).

The weakening of India’s saving culture is further aggravated by recent shifts in tax policy. Historically, the Indian tax framework encouraged saving by providing deductions under sections such as 80C, 80D, and incentives on home loans and provident fund contributions. These provisions acted as nudges, pushing families to save before they spent. The introduction of the new tax regime, however, turns this logic on its head. By offering lower tax rates only when citizens forgo these saving-linked deductions, the government is implicitly encouraging people to prioritise spending over saving. This shift is problematic in a country where financial literacy remains uneven and where saving was often enforced through structural incentives rather than voluntary discipline. As disposable income increases without the guardrails of tax-linked saving, spending naturally rises while savings fall.

What makes this situation particularly alarming is that the middle class and low-income groups—who make up the majority of India’s population—are disproportionately affected. Unlike the wealthy, who invest in equities, real estate, and global markets, ordinary families depend primarily on fixed deposits, post-office schemes, provident funds, and traditional insurance. When interest rates on these instruments decline and when tax incentives are diluted, these households lose both the motivation and the ability to save adequately. Meanwhile, the wealthy benefit from low interest rates because borrowing becomes cheaper and asset prices rise. This divergence in opportunity widens the gap between those who can grow wealth and those who watch their savings stagnate.

The erosion of the saving culture is also pushing India toward a dangerous dependency on debt. Low interest rates are often used as a policy tool to stimulate consumption, but in a society without strong social security systems, easy credit can quickly become a trap. Young people are increasingly adopting consumption-driven lifestyles—EMIs for phones, bikes, travel, and lifestyle purchases have become normalized. Instant digital credit apps have made borrowing easier than ever, often without borrowers fully understanding the long-term implications. As a result, India is witnessing the rise of a generation that spends more than it saves, borrows more than it invests, and is left financially exposed during emergencies. This gradual transition from a savings-based economy to a debt-fueled one carries long-term risks, including reduced resilience against economic shocks and weaker intergenerational wealth transfer.

Culturally, this is a significant shift. India’s earlier generations saved first and spent later. Today’s youth, shaped by the economic environment around them, are being nudged into doing the opposite. But this change is not due to a lack of discipline or values; it is being engineered by structural policy choices that make saving unrewarding and spending effortless. With rising inflation, stagnant wages in several sectors, and increasing costs of education, healthcare, and housing, the reduced returns on savings only make it harder for young families to build the financial cushions that were once considered essential.

If these trends continue unchecked, the consequences for the next generation will be severe. Household wealth accumulation will slow dramatically, making it difficult for families to achieve milestones such as home ownership, quality education for children, or secure retirement. Personal debt will rise, especially among young professionals who may already be juggling education loans, lifestyle EMIs, and high living costs in urban centres. Economic vulnerability will increase as families lose the safety net that traditional savings once provided, leaving them dangerously exposed to job losses, health emergencies, and market downturns. The intergenerational promise of upward mobility—a hallmark of India’s development story—may be broken, replaced by stagnation or even backward movement.

To prevent such an outcome, India must urgently rethink its policy direction. Restoring the saving culture requires a multi-pronged approach, beginning with safeguarding real returns for savers. Interest rates on small-saving schemes and government-backed deposits should be aligned with inflation so that household wealth does not erode over time. Tax incentives for long-term savings must be strengthened in both tax regimes, not weakened. A national strategy on household financial security—with stronger social protection systems, compulsory saving mechanisms, and widespread financial education—is essential. Above all, policymakers must recognize that household savings are not a barrier to economic growth but a pillar of national stability.

India’s economic future depends not only on GDP numbers but on the financial health of its families. If the policies that shape savings, taxation, and consumption continue in the current direction, the next generation will inherit a fragile foundation—one built on declining savings, rising debt, and dwindling security. A society that discourages saving is one that undermines its own future. India must act now to restore the culture of thrift and financial responsibility that once formed the bedrock of its economic strength.

(The author is freelance writer and trainer, brings rich insights into the intersection of finance and economics through his research & writing with a strong background in business studies & corporate analysis.)

Indian National Congress

AICC Hq, Indira Bhawan, 9A Kotla Marg, New Delhi - 110002